![By fernost (Self-photographed) [Public domain], via Wikimedia Commons](http://thegreatrecession.info/blog/wp-content/uploads/OilBarrels-500x375.jpg)

Oil today plunged quickly below $40 per barrel, taking oil prices down more than 20% from their high a little over a month ago. That officially defines a bear market in oil. As of today, oil has also moved below its 50-day, 100-day and 200-day moving averages. July has again turned out to be a huge disappointment for oil producers who mistakenly thought price recovery had come to stay.

In addition to the dark clouds I presented last week, here is a list of newly developing reasons and ways that oil prices are continuing to slide toward $30 per barrel … as I’ve predicted all along:

- Saudi Arabia today lowered its price of oil to Asia in order to compete more fiercely for market share, offering its biggest discount in almost a year … because the kingdom is now backed up with oversupply in its own tanks that it has to move. After raising prices to Asia not long ago, Saudi Arabia’s optimism about increased Asian demand proved short-lived.

- Asian refineries are lowering their production. According to Bloomberg, some are cutting refinery production by as much as 50%.

- Short positions for West Texas Intermediate crude (WTI) increased last week by their largest volume on record. Likewise with short positions on gasoline. Hedge funds in particular are betting on a gasoline glut. Summarized Newsmax, “Money managers have never been more certain that oil prices will drop.”

- The global economy is simply exhausted. Growth in global demand for oil continues slowing, and many nations and people simply cannot afford high oil prices any longer.

- Thanks in part to Brexit, the global petrodollar continues to rise in value, meaning it takes fewer dollars to buy a barrel of oil.

- Iran is expected to approve new oil contracts this week that will substantially open the doors to foreign investors in its oilfields, which will improve its supply capacity in years to come.

- OPEC’s production is expected to reach its highest output in recent history. Throughout 2016, the experts talked about how Saudi Arabia and Russia would reach a deal, how OPEC would soon start tapering back its supply. All along, I said “baloney! There will be no such agreement and no cutback by OPEC.”

- Libya is now back in the oil business.

- Gasoline inventories increased yet another week, now five out of six weeks during the busy summer season when gasoline inventories should decline. Soon seasonal driving will start to fall off, increasing the rate at which gasoline inventories build. As a result, US refiners are already dialing back gasoline production, which reduces demand for already oversupplied crude. Some reports have said refiners are beginning their autumn maintenance season early because they have more gasoline than they need for the remaining summer. Normally summer output is not curbed until the end of August.

“Coming out of the summer, these tanks will still be full,” Mark Benigno, co-director of energy trading at INTL FCStone Inc. (Oilprice.com)

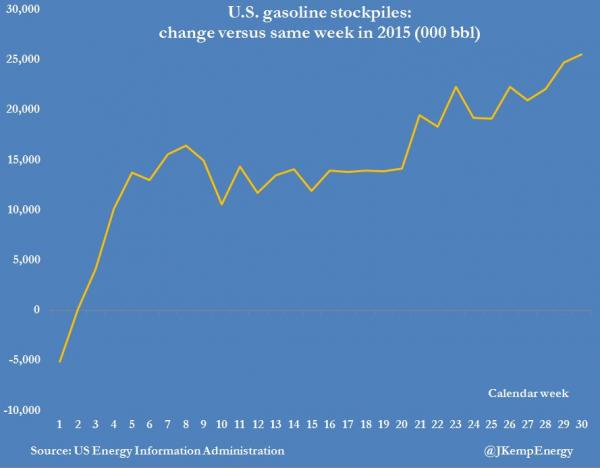

Here’s what gasoline stockpiles did this year compared to what stockpiles did last year:

Growth in oversupply in US gasoline stockpiles for 2016 compared against 2015.

Stockpiles of crude and gasoline are now at their highest summer level in two decades.

“The rise in supplies will add more downward pressure,” said Michael Corcelli, chief investment officer at Alexander Alternative Capital LLC, a Miami-based hedge fund. “It will be a long time before we can drain the excess.” (Bloomberg)

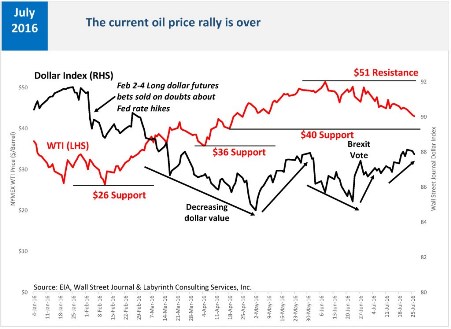

The downward oil price trend continues its impact on the global oil industry

There is a lot of price support — both psychological and on the charts — at $40, so that’s tough resistance to break. I wouldn’t be surprised, then, if oil prices bounce back upward as people buy the dip; but that speculative reaction is not likely to overcome the greater forces outlined above. If oil prices crash easily through the $40 floor, as just happened today, and they sustain that breakthrough, the trip down should accelerate. Below $36 per barrel there is no support all the way down to $26.

Points of major price support based on recent history of oil prices.

“The bottom line is the street has gotten it wrong as far as the oil markets achieving supply-demand balance this year…. We will likely break through the $40 levels in days and weeks to come,” said Tariq Zahir, crude trader and portfolio manager at Tyche Capital Advisors in New York. (Reuters)

That was last Wednesday. Now we can say, “been there, done that, on our way to thirty.” When I stated $30, prices were at $43, and $40 oil just seemed like too easy of a bar to clear in spite of its price support on the charts.

But the importance of all of this is its extreme impact:

Exxon, Chevron, Valero, BP, Royal Dutch Shell have all reported falling profits or even losses that disappointed the expectations of economists. (Chevron reported its largest quarterly loss in fifteen years. Exxon reported a 59% drop from last year. Shell, a 72% plunge, missing the estimates of the experts by over a billion dollars.) And this was the good quarter when oil prices were recovering.

“This is a very big surprise from Shell,” Brendan Warn, a managing director at BMO Capital Markets, told Bloomberg in an interview. “Things are not looking up in the third quarter either, with weakness in the industry’s refining environment and Shell’s oil production still under pressure.” (Oilprice.com)

All the big economists and oil analysts were predicting that a rebalancing of the oil market would be firmly in place by the second half of 2016. Now they are all revising their predictions to align with those that I continuously stated against the odds when prices kept rising.

2016 had such a promising start. Whether you listened to government agencies, banks, analysts, oil companies, or the oil-producing countries you would have heard the same message — the market will begin to rebalance in the second half and inventories will start to fall as rising demand overtakes dwindling supply…. It hasn’t quite worked like that. Demand has not surged as producers had hoped, and supply has proven more resilient than expected. Demand growth is slowing from its lofty levels earlier this year, dashing hopes that the supply will get soaked up quickly. But the real story is the supply outlook. There’s little cause for optimism here, at least in the short term…. We’re still seeing additional supplies from projects that were sanctioned in an era of much higher prices…. The result is a delay in the start of a long-waited rebalancing. The pickup in prices to above $50 a barrel in June looks to have been a false dawn. The price recovery is not yet here. So, if not now, when? Russian oil minister Alexander Novak suggests the market may now reach balance by mid-2017. (Newsmax)

And the importance of all of that is its impact on banks an on the general economy.

As I said last week, something dark this way comes from the oil sands and tar pits.