![By Federalreserve (00491) [Public domain], via Wikimedia Commons](http://thegreatrecession.info/blog/wp-content/uploads/US-Federal-Reserve-Eccles-Building-1937-500x378.jpg) We just saw a major rift open in the US stock market that we haven’t seen since the dot-com bust in 1999. While the Dow rose by almost half a percent to a new all-time high, the NASDAQ, because it is heavier tech stocks, plunged almost 2%. Tech stocks nosedived while others rose to create new highs. Is this a one-off, or has a purge begun for the tech stocks that have driven the nation’s third-longest bull market?

We just saw a major rift open in the US stock market that we haven’t seen since the dot-com bust in 1999. While the Dow rose by almost half a percent to a new all-time high, the NASDAQ, because it is heavier tech stocks, plunged almost 2%. Tech stocks nosedived while others rose to create new highs. Is this a one-off, or has a purge begun for the tech stocks that have driven the nation’s third-longest bull market?

Yesterday’s dramatic “rotational” divergence between tech stocks and the rest of the market, which as Sentiment Trader pointed out the only time in history when the Dow Jones closed at a new all time high while the Nasdaq dropped 2% was on April 14, 1999, stunned many and prompted Bloomberg to write that “a crack has finally formed in the foundation of the U.S. bull market. Now investors must decide if any structural damage has been done.” (Zero Hedge)

This is important because, without the nearly constant lead of those tech stocks, the market would have been a bear a long time ago. Tech stocks created half of the market’s gains in 2017. Financials, which led the Trump Rally, also hit the rocks in recent weeks, at one point erasing almost all of their gains for 2017, though they recovered a little of late. If both continue to falter, the rally rapidly implodes and maybe the whole bull market with it.

The Tech sector suffered its worse high-altitude nose bleeds at the end of May — the biggest outflow in over a year. Said Miller Tabak’s Matt Maley in a note to clients:

Everybody remembers 2000, so they might be getting a little nervous with this development. I just wonder how many people have said to themselves, ‘If AMZN gets to $1,000, I’m going to take at least some profits. (Zero Hedge)

Last Friday, of course, may be a one-off, but it may also be happening because central banks are pulling the plug on their direct ownership of the stock market or, at least, their hoarding of tech stocks. That direct cornering of the stock market largely went unnoticed until this past quarter. Central banks now have enough interest throughout the US stock market to be considered as having cornered the entire stock market, which means they have the capacity to let it fall or to keep it where it is by just refusing to sell their own stocks.

Have central banks rigged the stock market entirely?

Whether or not the market implodes now depends entirely on whether central banks let it fall. If they decide to continue to buy up all the slack, they may be able to keep it artificially afloat a lot longer because they can create infinite amounts of money so long as they keep it all in stocks so that it only creates inflation in stock values, as it has been doing, and not in the general marketplace. We have certainly seen that not much of it trickles from Wall Street down to Main Street. So, there is little worry of creating mass inflation from mass money printing.

I have long suspected that central banks were the only force preventing the crash of the NYSE that I predicted for last year and that started last January, which was the worst January in the New York Stock Exchange’s history. Last week, however, was the first time I read something that indicates I was right about the Fed propping up the stock market in order to take us through an election year by the extraordinary means of buying stocks directly.

In an article titled “Central Banks Now Own Stocks And Bonds Worth Trillions – And They Could Crash The Markets By Selling Them,” Michael Snyder writes,

Have you ever wondered why stocks just seem to keep going up no matter what happens? For years, financial markets have been behaving in ways that seem to defy any rational explanation, but once you understand the role that central banks have been playing everything begins to make sense…. As you will see below, global central banks are on pace to buy 3.6 trillion dollars worth of stocks and bonds this year alone. At this point, the Swiss National Bank owns more publicly-traded shares of Facebook than Mark Zuckerberg…. These global central banks are shamelessly pumping up global stock markets, but because they now have such vast holdings they could also cause a devastating global stock market crash simply by starting to sell off their portfolios…. The truth is that global central banks are the real “plunge protection team”. If stocks start surging higher on any particular day for seemingly no reason, it is probably the work of a central bank. Because they can inject billions of dollars into the markets whenever they want, that essentially allows them to “play god” and move the markets in any direction that they please. But of course what they have done is essentially destroy the marketplace. A “free market” for stocks basically no longer exists because of all this central bank manipulation. (The Economic Collapse Blog)

It is no secret, of course, that central banks were attempting to create a wealth effect by pumping up stocks through their own member banks — buying US bonds back from banks with free overnight interest with the proviso that banks use the income to buy stocks. As I wrote during last year’s stock market plunge, even central bankers finally admitted to that.

What is a secret is the fact that they have started buying stocks directly in order to pump up stock indexes. Federal Reserve chair, Janet Yellen, began talking openly about the possibility of doing that last year when it became obvious that the stock market was failing, and I speculated that the Fed actually started to do what they were talking about covertly through proxies so it wouldn’t show up on their own balance sheet.

Those proxies could have been there own member banks, but it turns out to have been other central banks. Their ability to get other central banks to do that for them could go like this. “We’ll buy $100 billion of your bonds if you agree to buy $100 billion worth of stocks in the US stock market to help us keep this thing up through the election season.” (Replace bonds with whatever else that central bank may need to see happen in the economy that it manages.)

The Swiss National Bank is one of the biggest offenders. During just the first three months of this year, it bought 17 billion dollars worth of U.S. stocks, and that brought the overall total that the Swiss National Bank is currently holding to more than $80 billion.

Have you ever wondered why shares of Apple just seem to keep going up and up and up?

Well, the Swiss National Bank bought almost 4 million shares of Apple during the months of January, February and March.

I wonder how many it bought last year when the stock market needed a recovery team. And that’s just one of the Fed’s friends, who was ready to rush in so as to suppress the Swiss franc. These banks are now following the Chinese model of crash protection. This is exactly what China’s central bank did on a massive scale to prop up its failing stock market and end the crash. It essentially nationalized many of its companies by soaking up all the slop in stocks.

Will central banks now let the rigged stock market crash?

If I was right about the Fed shoring up the stock market through proxies — and it appears now that I was — I also said all of last year that they would most likely only do that long enough to make sure Obama’s team won the election. If their recovery was failing as bad as I believed it was, I figured they’d do anything they could to continue to hold it up long enough to make get Team Obama (Hillary) elected. Trump, during his candidacy, was talking a lot about how Janet Yellen needed to go. So, you know the central bank would definitely want to keep Trump out of power. I noted how the Fed held mysterious closed-door emergency meetings last year, including one immediately called with the president and vice president.

Also, if it became clear to them that their recovery was going to fail, they wouldn’t want their globalist friend, Obama, to take the blame — being globalists themselves — and certainly wouldn’t want themselves to take the blame for a recovery that failed the moment they pulled the stimulator’s plug out of the wall. They’d need a scapegoat, and they would love for it to look like the crash was entirely the fault of anti-globalists. So, their private motto, should Trump win, would be “Trump for Chump” if they knew everything was hopeless (as I’ve been saying it is for a long time because their recovery plan was always a horrible solution).

Now that Trump has stocked his cabinet with Goldman Sachs Execs., however, Trump talks a completely different story about Yellen. She’s good now and valuable, and he says he’d like to see more loose monetary policy, so their reasons to eject him may be less pronounced; but, at the time, they didn’t know for sure if they could own him. And it may be all the more clear to them at this point that their recovery is going to fail as soon as they stop propping up stocks.

Now that it’s clear central banks have been buying enormous flows of US stocks, this could explain why the stock market paradoxically rose right after the Fed announced its rate hike in March. Mysteriously, stock prices made their third largest post-FOMC meeting move upward right after their announced rate hike, an event that would normally send stocks down. Even Goldman Sachs said they found the move mysterious. In fact, Goldman noted that stock prices rose as a result of the Fed’s quarter-point rate increase as they would normally be expected to rise had the Fed lowered its interest target by that much. Goldman’s analysis was that this was “almost certainly not” the central bank’s desired outcome.

Yes, “almost certainly not.” Perhaps I have an explanation for this mystery: The Fed appears now to have had friends in faraway places ready to backstop the market the second the decision was announced. I don’t know that’s what happened right at that moment, but we do know now that central banks have been directly supporting the US market this year and last with massive purchases. For their part, Goldman stayed with calling the event a mystery and said that the anomaly only meant the Fed would have all the more incentive to raise rates again at its next meeting.

I’m a little more suspicious than that and far less a friend of the Fed than Goldman, which practically owns the Fed. I always maintained that the Fed would discover it couldn’t raise rates twice without crashing it’s phony recovery. That, however, would not be true if they have friends of nearly infinite financial power waiting in the wings as the plunge protection team. I’m not as content as Goldman to leave it an unsolved mystery. So, I’m going to put out a hypothesis that goes from Goldman’s “almost certainly not” their intention to cause the market to rise to “Oh, I guess it was their intention”:

If you finally start to realize your recovery does not appear it is going to succeed — that it will never become capable of holding on its own — then you will really want the failure of your recovery to happen at a time when you can scapegoat someone else. One way to do that and not get blamed for the failure is to make sure you secretly give the market a huge jog with the right timing and severity to be sure it crashes on that person’s watch.

To do that clandestinely, have your friends lift the market upon your first rate hike that year. That way you make the rate hike when you know the market cannot fail because friends are ready to prop it up, and you prove to everyone you have full confidence in your recovery, even though the only thing you really have confidence in is your own confidence game. The fact that the market rises when everyone would have expected it to fall gives you lots of justification for another rate hike due to the market’s now “proven” resilience to rate hikes. Then, you make sure your friends don’t lift the market when you make your next rate hike. You’ll appear justified in making the hike, but the market will fall from a greater height because of its artificial lift from your friends with more force as it essentially corrects to what is now essentially a double rate hike (since the first one never got priced in) once the artificial lift is removed.

If that’s too jaundiced and conspiratorial for you, I’ll accept that criticism; but a year ago people probably thought I was overreaching in suggesting the Fed was propping up the stock market with direct purchases of stocks through proxies. While I cannot even yet prove the Fed had anything to do with US stocks being propped up that way, we do now know for certain they were propped up that way and to a very large degree. The Fed’s friends were extremely active last year in doing something that central banks, heretofore, were not known to do (outside of such moves within their own stock markets by Japan’s central bank and China’s):

Two weeks ago Bank of America caused a stir when it calculated that central banks (mostly the ECB & BoJ) have bought $1 trillion of financial assets just in the first four months of 2017, which amounts to $3.6 trillion annualized, “the largest CB buying on record.”(Zero Hedge)

We now know some of that enormous stimulus was spent on US stocks.

This time is different

I’m not saying, by the way, that the Fed has never purchased US stocks. We all know it bought lots of stock when it bailed out automakers and banks in the early days of the Great Recession. At the time, that was a peculiar thing to do, in and of itself; but the policy of soaking up slack in the stock market generally by buying perfectly sound companies as a form of economic stimulus is new in the US. In fact, it was so much something that simply wasn’t done (and should never be done) that the US central bank merely suggested it last year as a brave new approach should their recovery fail, should the economy need a new boost after quantitative easing had lost all of its utility due to diminishing returns and should we find ourselves in a recession. (Clearly proposed as a last-ditch effort.)

Well, having run that flag up the pole without hearing too much objection to the idea, is it too much to think that, when the market did fail badly last January, the Fed found other central banks willing to leap into that role for them? Why not? It was no secret that China’s move of that sort was the only thing that saved China’s stock market (though it also made it no longer a true market by effectively nationalizing many of China’s corporations).

Of course, the Federal Reserve could own stocks directly that are hiding within some broad category on its balance sheet as well as any stocks that it still holds from its direct bailouts. They have already begun talking about starting the unwind of their massive balance sheet this year. If that includes an unwind of stock purchases, it will certainly bring the market down in Trump’s first year. If the Fed isn’t planning a stock-market failure by conspiracy, the question remains, will the Fed allow the stock market to fall even if they are just becoming aware their recovery won’t hold?

While normally we would caution that the Fed may simply step in during any concerted selloff amid the broader market (catalyzed by the tech sector) as it has every single time in the past, this time it may let gravity take hold: after all, not only did the Fed caution during its last FOMC minutes that elevated asset prices have resulted in “increased vulnerabilities” and that “asset valuation pressures in some markets were notable” but as Goldman also warned recently, Yellen may be looking for just the right “shock” with which to reaffirm control over a market which is now interpreting a rate hike as an easing signa (see “Goldman Asks If Yellen Has Lost Control Of The Market, Warns Of Fed “Policy Shock”) (Zero Hedge)

On the conspiratorial side, that may just be the Fed’s best friend, Goldman Sachs, helping create the excuse the Fed needs for letting the market go. Why would Goldman want that? Well, so long as Goldman casts its bets against the market, they (and maybe this time their clients) could reap large rewards if the Fed lets the market go. They’d come out like champs.

If the Fed’s recovery plan failed too soon after Trump’s inauguration,however, people would not automatically blame him, and any conclusion people reach on their own is far stronger held. That’s how a confidence game works. If the market fell right after he was inaugurated, people would possibly see it as a mess he inherited. If the failure was seen as something baked in during the Obama administration, the Fed would have to own its own abject failure because the Obama administration reigned throughout the Fed’s recovery program. Moreover, if the Fed’s recovery failed during the Obama administration, Trump’s victory would be certain because America always votes it pocketbook.

For the Fed and the globalists to hope to dodge all blame, Trump would have to be in office long enough to do enough or fail enough for people to say, “This is clearly your fault.”

While that was all speculation when I was saying last year, it does seem to be the way things are playing out. And now that it is clear central banks have been soaking up massive amounts of US stocks, it’s a little more than just speculation.

Putting conspiracy aside, this market still looks like it is falling right when I predicted it would

Whether by conspiracy or sheer blindness and idiocy, the Fed is about to raise rates right into a falling economy. GDP in the first quarter went really soft, and I believe, contrary to what the Fed projects, second quarter GDP will come back negative unless great massaged. (In fact, first quarter GDP may have been negative if it were not such a government-manipulated number in the first place.)

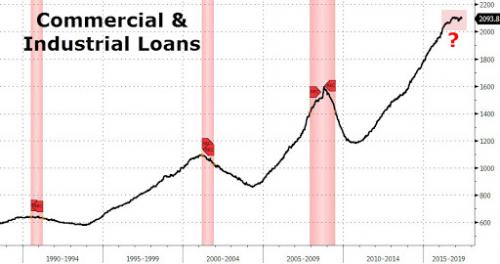

One indicator has remained a stubbornly fail-safe marker of economic contraction: since the 1960, every time Commercial & Industrial loan balances have declined (or simply stopped growing), whether due to tighter loan supply or declining demand, a recession was already either in progress or would start soon…. As US loans have failed to post any material increase in over 30 consecutive weeks, suddenly the US finds itself on the verge of an ominous inflection point. After growing at a 7% Y/Y pace at the start of the year, which declined to 3% at the end of March and 2.6% at the end of April, the latest bank loan update from the Fed showed that the annual rate of increase in C&A loans is now down to just 1.6%, – the lowest since 2011. Should the current rate of loan growth deceleration persist – and there is nothing to suggest otherwise – the US will post its first negative loan growth, or rather loan contraction since the financial crisis, in roughly 4 to 6 weeks. (Zero Hedge)

Why is loan growth finally slowing again? Simple. GDP and loan growth are showing us something that a rigged stock market cannot and will not. The Fed started raising interest rates, and immediately applications for new home mortgages and auto loans started to subside, and the recovery started to falter … just as I said would happen more than a year ago. I’ve maintained all along that the Fed cannot raise interest rates (reduce its economic stimulus) without crashing its recovery (that, however, was without foreseeing when I first said it that they would prop things up via their potent proxies for a short time because that is simply moving central-bank stimulus from being overt to being covert).

Of course, another significant factor that helped the Fed raise interest rates in March was the fact that the financial market was already ahead of them. Interest was rising on its own purely out of speculation over the Trump effect, wherein markets were repositioning (or, at least, appeared to be) for the anticipated fiscal stimulus of Trump’s big tax cuts and the huge debts to be created by his infrastructure spending plans. (However, we also now know the market was rising due to enormous central bank stock purchases. No wonder the rally was so steep, but that now appears to be all unwinding.)

The Fed has a history of knee-capping its own recoveries by raising interest just as the economy is getting wobbly in the knees anyway, so we should not be surprised (even from a non-conspiratorial outlook) if the Fed fails to see its recovery is crashing all around it and raises rates directly into failure.

Just recall how Ben Break-the-banky failed to see the last recession when he was standing right in the middle of it. The Fed has a peculiar talent for that. Sometimes I think conspiracy rises as the most likely answer only because its so hard to be believe that people who are that smart can be that stupid. Yet, Gentle Ben was either supremely stupid in the area of his supposed greatest expertise, or was lying about the lack of recession, which often happens when people are conspiring. So, you choose — stupid or conspiratorial. Either one is still going to take this market down.